Real Estate Investment Trusts (REITs) and Infrastructure Investment Trusts (InvITs) have been listed on Indian exchanges since 2019, but a large part of the retail investing community still treats them as unfamiliar territory. That is changing. SEBI has made a series of regulatory changes in recent years that have steadily made these instruments more accessible to retail investors. This article covers what REITs and InvITs actually are, how each one works, how they are structured, and what the key regulatory framework looks like.

What a REIT Is

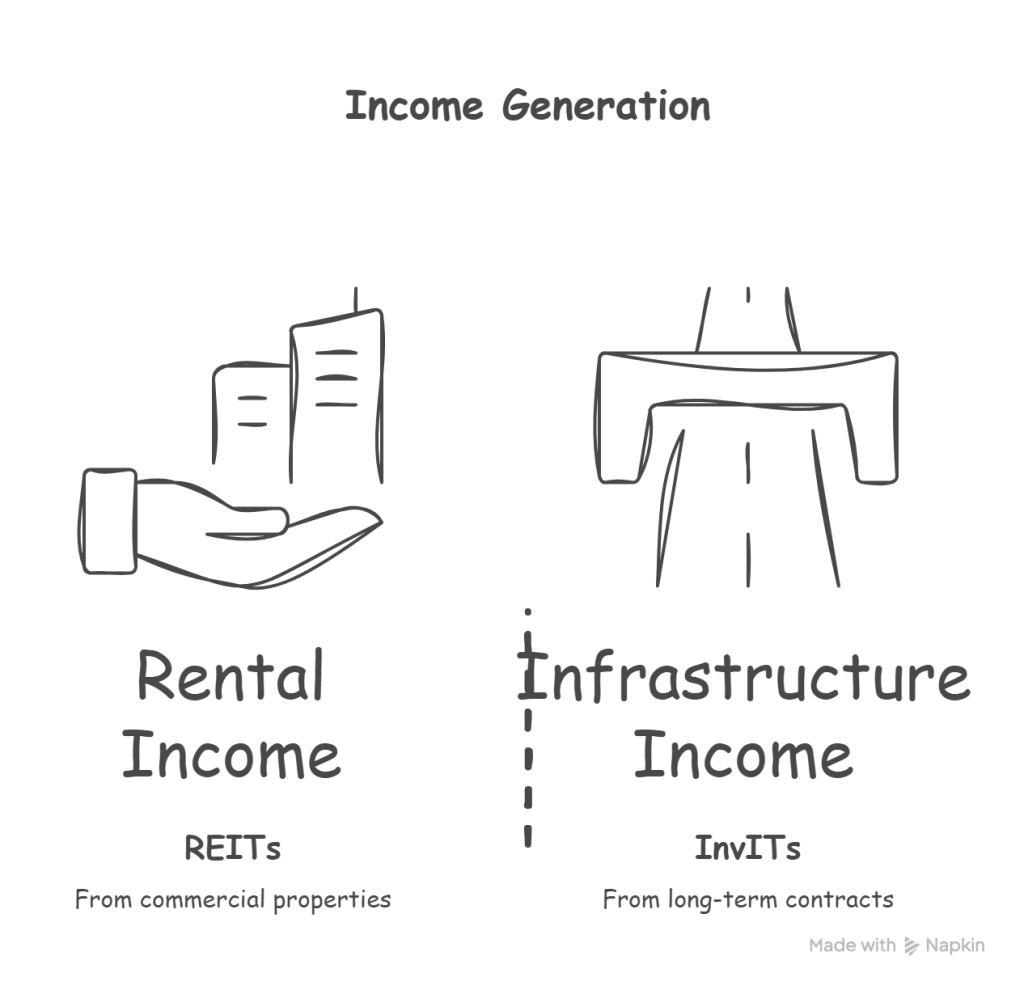

A Real Estate Investment Trust is a SEBI-regulated trust that pools money from investors to own and operate a portfolio of income-generating real estate assets. In India, REITs currently hold commercial real estate, primarily Grade-A office parks, with the exception of Nexus Select Trust which holds retail malls.

The trust collects rental income from tenants occupying these properties and distributes the majority of it to unitholders on a regular basis. REITs are required under SEBI regulations to distribute at least 90% of their net distributable cash flows to unitholders. At least 80% of a REIT’s assets must be in completed, income-generating properties. No more than 20% can be in under-construction assets.

SEBI has reclassified REITs as equity-related instruments, which means equity mutual fund schemes can now include REITs within their equity allocation limits. This significantly expanded the pool of institutional capital that can flow into the asset class and opens the door to potential inclusion in equity indices over time.

What an InvIT Is

An Infrastructure Investment Trust is a SEBI-regulated trust that pools money from investors to own and operate a portfolio of income-generating infrastructure assets. These include national highways, power transmission lines, gas pipelines, renewable energy parks, and telecom towers.

Revenue comes from long-term concession agreements, toll collections, power purchase agreements, gas transmission tariffs, and contracted infrastructure usage fees. Like REITs, InvITs are required to distribute at least 90% of distributable cash flows to unitholders.

At least 80% of an InvIT’s assets must be in completed, revenue-generating infrastructure projects. SEBI amendments have progressively allowed InvITs to allocate a portion of assets in under-construction or greenfield projects, with the most recent changes extending this flexibility to privately placed InvITs as well.

Unlike REITs, InvITs remain classified as hybrid instruments by SEBI. This means they count within the hybrid allocation headroom for mutual fund schemes rather than the equity allocation bucket.

The Key Structural Difference Between the Two

The simplest way to understand the difference is through what the underlying assets generate. REITs generate rental income from tenants occupying commercial or retail properties. The income is tied to lease agreements, occupancy rates, and rent escalation clauses. InvITs generate income from infrastructure concessions and long-term usage contracts. The income is tied to traffic volumes on roads, units of power transmitted, or volumes of gas transported.

REITs are more sensitive to commercial real estate demand cycles, office vacancy trends, and the pace of lease renewals. InvITs are more sensitive to government policy on infrastructure concessions, traffic projections, and tariff revision mechanisms. Both are sensitive to interest rate movements because they are yield-oriented instruments: when the RBI cuts rates, borrowing costs for the trust fall and valuations tend to improve.

How They Are Structured

Both REITs and InvITs operate through a trust structure. The trust holds assets either directly or through Special Purpose Vehicles (SPVs). An SPV is a subsidiary entity created specifically to hold one or more underlying assets, such as a single road project or a specific office building.

The trust is managed by an Investment Manager, which is a SEBI-registered entity responsible for making investment decisions and managing the portfolio. A Trustee, which must be independent from the Manager and Sponsor, holds the trust assets on behalf of unitholders and oversees compliance. The Sponsor is typically the entity that seeded the trust with initial assets, and Sponsor entities are subject to minimum holding and lock-in requirements under SEBI regulations.

How to Buy Them

Both REITs and InvITs are listed on NSE and BSE and can be bought and sold through a standard demat account during market hours, exactly like equities. The minimum trading lot size for publicly listed REITs and InvITs is 1 unit, which was reduced from earlier higher lot sizes specifically to improve retail accessibility.

For privately placed InvITs, which are not exchange-listed, SEBI has progressively reduced the minimum investment threshold over time, bringing it more in line with secondary market lot sizes. These changes have made private InvITs accessible to a wider category of investors beyond the institutional segment.

The Listed Instruments in India

The number of listed REITs and InvITs has grown steadily since the first listings. Currently, there are multiple publicly traded REITs and a larger number of InvITs listed on Indian exchanges. SEBI’s ongoing reforms are expected to expand this universe further.

The publicly traded REITs include:

Embassy Office Parks REIT (NSE: EMBASSY): India’s first and largest REIT. Sponsored by Embassy Group and Blackstone. Portfolio of commercial office space across Bengaluru, Pune, Mumbai, and Noida.

Mindspace Business Parks REIT (NSE: MINDSPACE): Sponsored by K Raheja Corp and Blackstone. Office parks in Mumbai, Hyderabad, Pune, and Chennai.

Brookfield India Real Estate Trust (NSE: BIRET): Sponsored by Brookfield Asset Management. Office campuses in Mumbai, Gurugram, Noida, Kolkata, and Delhi.

Nexus Select Trust (NSE: NXST): India’s first retail mall REIT. Sponsored by Blackstone. Portfolio of Grade-A shopping malls across multiple cities, plus hotel and office assets.

Among the established publicly traded InvITs:

IRB InvIT Fund (NSE: IRBINVIT): India’s first publicly listed InvIT. Focused on toll road projects across national highways. Revenue from toll collections.

India Grid Trust / IndiGrid (NSE: INDIGRID): Power transmission lines. Revenue from long-term transmission service agreements with electricity distribution companies.

PowerGrid Infrastructure Investment Trust (NSE: PGINVIT): Sponsored by Power Grid Corporation of India, a government entity. Revenue backed by government payment obligations on power transmission.

The list above reflects publicly traded instruments. Privately placed InvITs exist in larger numbers but are not accessible to retail investors on the exchange.

Distributions and Taxation

Distributions from REITs and InvITs are paid quarterly or half-yearly depending on the trust. The nature of the distribution determines how it is taxed in the hands of unitholders, and distributions can consist of multiple components: interest income passed through from SPVs, dividend income, rental income, and return of capital.

SEBI-registered REITs and InvITs issue Form 64B to unitholders at the end of each financial year, showing the full breakdown of the distribution into each income category. The tax treatment differs by component. Interest distributed is taxable as income from other sources. Dividends are taxable at applicable income tax rates. Rental income distributed where the REIT directly owns the property is taxable as rental income. Return of capital components are not taxable at the time of receipt but reduce the cost of acquisition of units, affecting capital gains calculations when units are eventually sold.

There is no minimum threshold for TDS deduction on distributions from REITs and InvITs.

What SEBI’s Recent Amendments Have Changed

SEBI has made multiple rounds of amendments to the REIT and InvIT regulatory framework in recent years. The broad direction of these changes has been consistent: reducing minimum investment thresholds, improving governance and disclosure standards, expanding the definition of eligible investors, and giving trusts more operational flexibility in how they manage assets and raise capital.

Key changes include the reduction of minimum investment thresholds for private InvITs, the reclassification of REITs as equity instruments for mutual fund purposes, streamlined valuation report submission timelines, relaxed borrowing norms for InvITs, and provisions allowing InvITs to hold SPV investments for longer after concession agreements end.

The regulatory framework continues to evolve. SEBI’s stated goal is to align Indian REIT and InvIT regulations progressively with global best practices while strengthening investor protection.

What These Instruments Are Not

REITs and InvITs are not fixed deposits or bonds, even though they pay regular distributions. The distribution amount is not guaranteed and can vary based on the operating performance of the underlying assets. Unit prices on the exchange fluctuate based on market conditions, interest rate movements, and the performance of the underlying portfolio.

They are not direct real estate or infrastructure ownership. A unitholder owns units in a trust that holds these assets, not a fractional claim on specific properties or roads.

They are also not equivalent to real estate developer stocks. Developer stocks are exposed to project execution risk, sales volumes, and balance sheet leverage. REITs hold completed, income-generating assets managed by professional operators under SEBI oversight, which is a structurally different risk profile.

Both REITs and InvITs are traded on NSE and BSE and can be bought through any standard demat and trading account. The Nifty REITs and InvITs Index tracks the combined performance of listed instruments in both categories.

Disclaimer: The information provided in this article reflects the regulatory framework and listed instruments available at the time of writing. SEBI regulations governing REITs and InvITs are subject to change, and the list of listed instruments may expand or change over time. Readers are encouraged to verify current regulations and instrument details before making any investment decisions.